The calculations Musicality did in order to switch to ABC revealed that the Solo product was generating a loss for every unit sold. Musicality could also decide to continue selling Solo at a loss, because the other products are generating enough profit for the company to absorb the Solo product loss and still be profitable. Why would a company continue to sell a product that is generating a loss? Sometimes these products are ones for which the company is well known or that draw customers into the store.

Products

Over the period, we have performed one thousand configurations, which gives us EUR 250 per machine set-up. The ABC approach helps us seggregate costs to fixed, varible and overheads. Whenever products use the same resources in ther production cycle, but use them in a different matter, some weighing is needed.

Promoting efficiency and cost savings

- Over the period, we have performed one thousand configurations, which gives us EUR 250 per machine set-up.

- The ABC method is a costly approach that recognizes the relationship between produced goods, costs, and overheads.

- Our website services, content, and products are for informational purposes only.

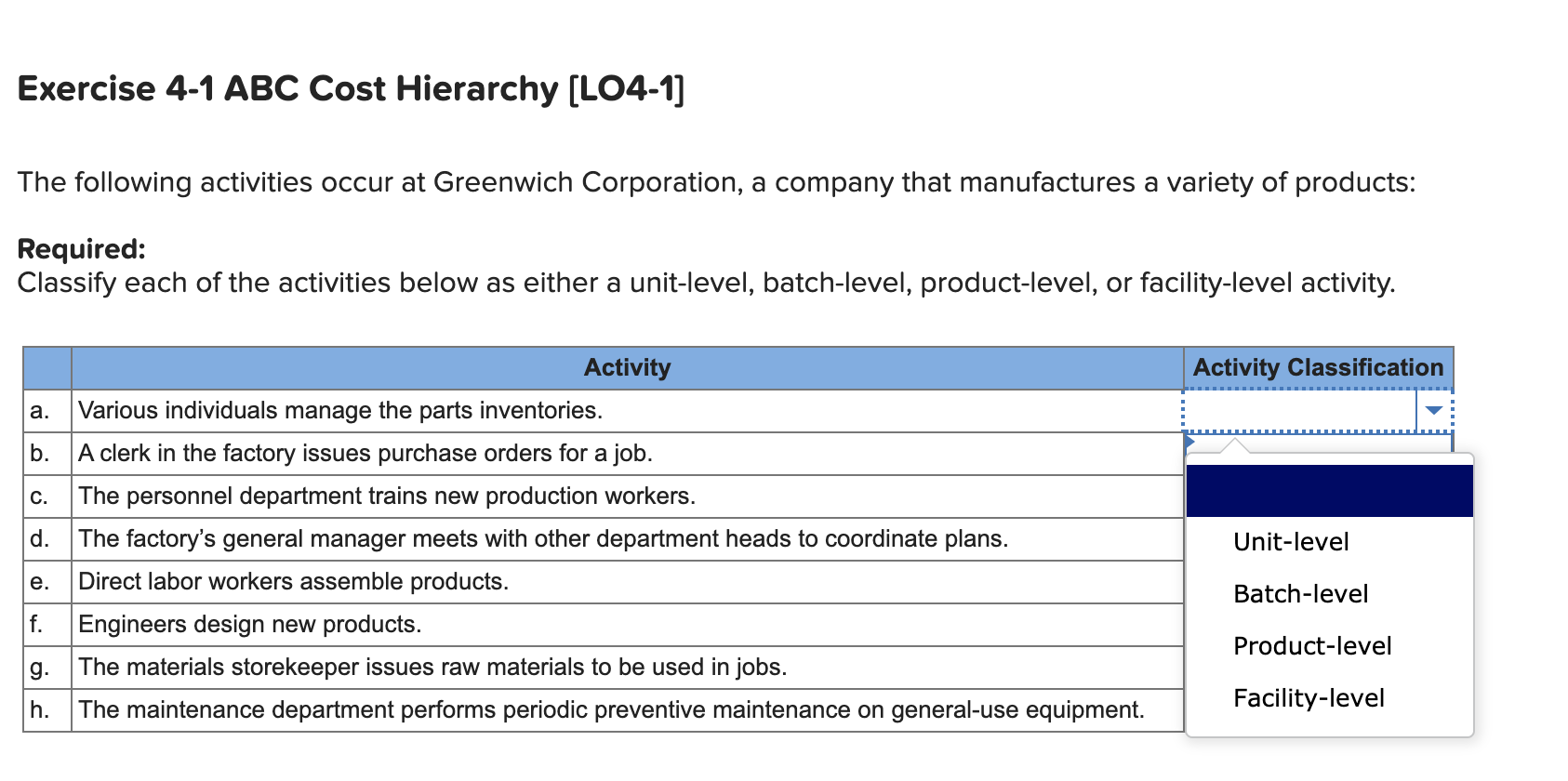

- The levels are (a) unit level, (b) batch level, (c) product level, and (d) facility level.

The robotics function related to the operation of the highly automated assembly line. A large part of the cost of robotics was tied directly to the number of units produced. The company was required to set up the assembly process for each batch of caps and glasses.

Accounting for Managers

The primary difference between activity-based costing and the traditional allocation methods is the amount of detail; particularly, the number of activities used to assign overhead costs to products. In practice, companies using activity-based costing generally use more than four activities because more than four activities are important. Activity‐based costing assumes that the steps or activities that must be followed to manufacture a product are what determine the overhead costs incurred.

This can, again, bias the cost allocation and present a distorted picture of the financials. Using an appropriate activity base not only ensures accurate and credible reporting, but it can also help companies identify inefficiencies in their processes. For example, if resource batch-level activity usage per unit of the activity base is high compared to industry benchmarks or historical averages, it might indicate areas where processes can be streamlined or waste can be reduced. This can lead to operational and cost efficiencies, further promoting sustainability.

To accurately identify the most suitable activity base for your business operations, there are various key factors to take into account. Platinum Interiors recently placed an order for 150 units of the 6-set type. Since it is a customized order, Platinum will be billed at cost plus 25%. Kohler defined an activity as a portion of work done by a specific part of the company. By tracking the costs of such activities in various parts of the company, Kohler began the precedent of accounting for the cost of work activities. A business might have dozens of cost objects, hundreds of activities, and numerous resource pools to evaluate.

Robin Cooper and Robert S. Kaplan, proponents of the Balanced Scorecard, brought notice to these concepts in a number of articles published in Harvard Business Review beginning in 1988. Cooper and Kaplan described ABC as an approach to solve the problems of traditional cost management systems. These traditional costing systems are often unable to determine accurately the actual costs of production and of the costs of related services.

Hence, tactful communication that provides comprehensive context is crucial when conveying such changes. Capturing costs with ABC using activity base information often leads to more transparent pricing. This transparency can prove beneficial for maintaining trust with customers. When consumers understand how costs are apportioned, they are more likely to perceive the prices as fair, building a stronger relationship with the business.

The other costs were either deemed attributable to one of the four activities, or otherwise not allocated. This costing system is used in target costing, product costing, product line profitability analysis, customer profitability analysis, and service pricing. Activity-based costing is used to get a better grasp on costs, allowing companies to form a more appropriate pricing strategy. To choose an appropriate activity base, companies can perform a thorough analysis of their internal operations and external industry norms.